A Decade of Structural Change for Natural Gas

The global natural gas market is entering a phase of structural change. According to the International Energy Agency’s (IEA) recent report “Gas 2025: Analysis and Forecasts to 2030,” a significant wave of new liquefied natural gas (LNG) capacity is underway that could reshape global price dynamics, trade flows, and supply strategies.

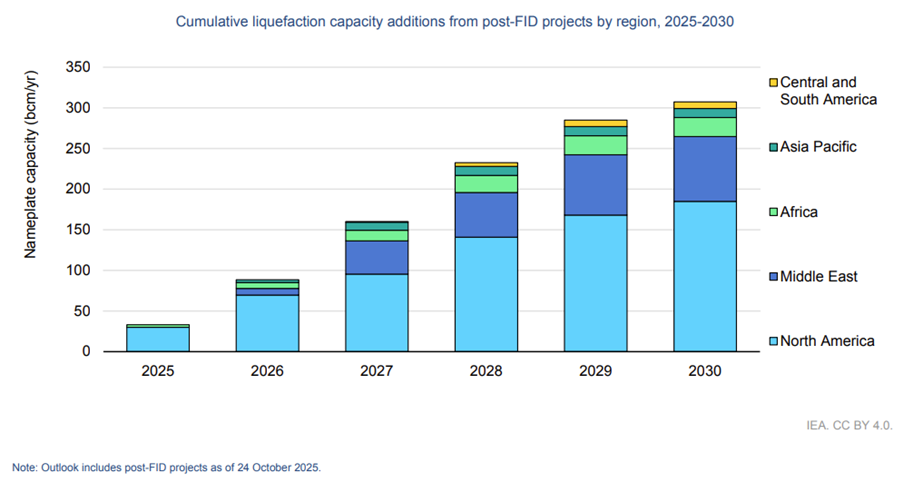

Between 2024 and 2030, around 300 billion cubic meters per year (bcm/y) of new liquefaction capacity is expected to be incorporated; an unprecedented expansion led by the United States and Qatar, which together will account for more than 70% of the global increase.

This massive expansion promises to improve global energy security and reduce price volatility following the shocks of 2022–2023. However, it also introduces new challenges, including risks of temporary oversupply, contractual tensions, and the need to adapt infrastructure and decarbonization policies.

Demand: Moderate Growth and Shifting Geography

The IEA forecasts global gas consumption to grow by around 1.5% per year through 2030, equivalent to an added +380 bcm. However, this growth will not be evenly distributed across regions:

- Asia-Pacific will account for most of the expansion, driven by rising demand in China, India and emerging Southeast Asian economies.

- Europe is expected to reduce gas consumption by around 8% until 2030 compared to pre-2022 levels, reflecting ongoing electrification and the shift toward renewable energy.

- The Middle East and Africa are expected to increase their use of gas as a vector for industrialisation and electricity generation.

Global Gas Demand Growth by Region (2024–2030)

The Supply Side: U.S. and Qatar Redraw the Global LNG Map

Strengthening global liquefaction capacity will significantly reshape LNG export dynamics.

The United States is projected to increase its share of global LNG supply from roughly 20% in 2024 to more than 30% by the end of the decade, reinforcing its role as the world’s leading exporter. Qatar, for its part, is moving forward with the expansion of its North Field project, which will add more than 60 bcm/y of capacity.

Together, these projects provide a safety cushion of supply, but they may also lead to periods of temporary oversupply, particularly between 2026 and 2028, before new Asian demand is fully realized.

According to the IEA, 65 bcm of surplus could remain in the baseline scenario if new regasification infrastructure and local distribution networks in Asia do not develop quickly enough.

Prices and Trade Flows: Toward a New Stage of Flexibility

Spot gas prices stabilized in 2025. Increasing LNG liquidity and the entry of more flexible contracts are contributing to greater price convergence across regions and Benchmarks.

The IEA points to a structural shift in contracting: long-term contracts continue to dominate, but now include more flexible volumes and a higher share of gas-hub indexation rather than oil indexation. This evolution will ease the reallocation of cargoes during demand shocks or geopolitical disruptions, strengthening overall market resilience.

Risks and Challenges: Infrastructure, Investment and Geopolitics

The main risk of the new LNG cycle is not a shortage of gas, but the lack of infrastructure. Many emerging countries still lack adequate regasification terminals, pipelines or storage systems. The IEA estimates that a quarter of the potential growth in Asian demand may not materialise due to this lack of infrastructure.

Another concern stems from LNG’s own success: prolonged periods of low prices could discourage new upstream investments, creating an upward imbalance after 2030. Additionally, geopolitical and technical risks — including sanctions, maintenance issues or incidents at large plants — may continue to strain supply and cause episodes of market volatility.

Decarbonisation: Transforming the Global Gas & LNG Chain

The report devotes special attention to reducing the carbon footprint of the gas and LNG chain.

Carbon capture, use, and storage (CCUS) technologies are gaining traction, especially in liquefaction and gas processing plants. Integrating these solutions can offer a competitive advantage in markets where the carbon footprint is beginning to condition contracts and financing. When it comes to low-emission gases, the report projects that global production of biomethane, low-emission hydrogen and e-methanol / e-methane is expected to increase 2.5-fold by 2030 but will still account for less than 1% of total gas supply.

The impact of these gases will be modest in the short term, but strategic in the medium term for the decarbonisation of gas and the diversification of energy portfolios.

Conclusion

In short, the LNG “wave” redefines the global gas sector. The abundance of supply expected during the second half of the decade will bring more competitive prices and energy security, but it will also introduce greater commercial and technological complexity.

Companies that know how to anticipate these changes — by optimizing contracts, investing in infrastructure, and reducing their carbon footprint — will be best positioned to turn the energy transition into an opportunity for long-term growth.

For more information on how to navigate these challenges, or to understand the evolution and development of the LNG supply chain and its impact on energy prices locally, in Europe and globally, please do not hesitate to contact us via https://www.nusconsulting.com/es/.